Figuring out how much you need to retire comfortably is like trying to hit a moving target. One day, you hear you need a cool million in the bank, the next day, it's two million. It's enough to make your head spin!

According to the AARP Financial Security Trends Survey, 61% of Americans 50 and older are worried they won't have enough money for retirement.

Without a clear goal, you might end up working longer than you want, pinching pennies when you should be enjoying life, or worse, running out of money when you least expect it.

There will be no guesswork or anxiety anymore. We are going to tell just practical, actionable steps to figure out your magic retirement number.

What Factors Influence Your Retirement Savings Goal?

Your retirement savings goal is as unique as your fingerprint, shaped by a variety of factors that are specific to your life and circumstances.

Current Age and Desired Retirement Age

Your current age and desired retirement age play a huge role. The earlier you start saving, the more time your money has to grow through the power of compound interest.

Life Expectancy

Americans are living longer; according to the SSA's 2024 OASDI Trustees report, the period of life expectancy at age 65 is:

For males: 18.2 years (which would mean living to about 83.2 years old)

For females: 20.8 years (which would mean living to about 85.8 years old)

That means your retirement savings may need to stretch further than you think. So, it's wise to plan for a retirement that could last 20-30 years or more.

Lifestyle Expectations

A big part of deciding your savings goal is figuring out what kind of retirement lifestyle you want. Do you envision a quiet life in your current home, or are you planning extensive travel and new experiences? The more active and luxurious your retirement plans, the more you'll need to save.

Inflation

While often overlooked, inflation can significantly impact your retirement savings. Even a modest inflation rate of 2-3% per year can substantially reduce your purchasing power over time. It's essential to factor in inflation when calculating your retirement needs to ensure your savings keep pace with rising costs.

Healthcare Costs

Healthcare expenses often increase as we age and can take a big bite out of retirement savings. Healthcare costs in retirement can be substantial, often surpassing what many people anticipate. You've got to take medical expenses into account, including long-term care.

Location

Some areas have a much higher cost of living than others, affecting everything from housing costs to daily expenses. Consider researching potential retirement locations and their associated costs as part of your planning process.

Common Retirement Savings Benchmarks

It's natural to wonder, "Am I on track?" While everyone's situation differs, financial experts have developed some general guidelines to help you assess your progress.

The 4% Rule

One popular benchmark is the 4% rule. This rule suggests that if you withdraw 4% of your retirement savings each year, adjusted for inflation, your nest egg should last about 30 years. So, if you have $1 million saved, you could withdraw $40,000 in your first year of retirement.

However, this rule has its limitations. It assumes a 30-year retirement and a specific investment mix. You may need to change your withdrawal rate if you want to retire early or if you think you will live longer.

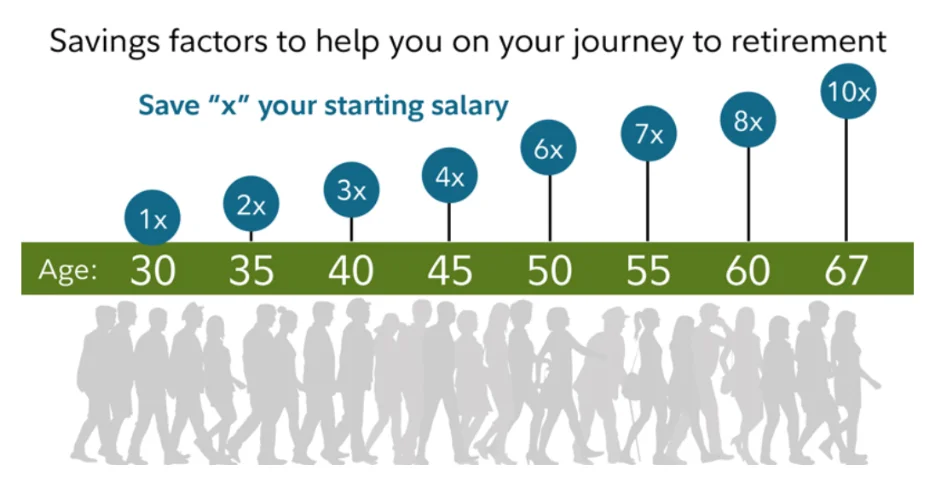

Retirement Savings Multiples

Another common benchmark is saving a certain multiple of your income by specific ages. Fidelity, a leading investment firm, recommends saving certain multiples of your income by specific ages:

1x your salary by age 30

3x by age 40

6x by age 50

8x by age 60

10x by age 67

(Fidelity’s salary multipliers, Source: Fidelity)

For example, if you earn $50,000 per year, you should aim to have $50,000 saved by 30, $150,000 by 40, $300,000 by 50, $400,000 by 60, and $500,000 by 67.

These multiples provide a rough estimate, but they don't account for factors like your expected lifestyle in retirement or other sources of income, such as Social Security or pensions.

The 80% Rule

Many experts suggest aiming to replace about 80% of your pre-retirement income. So, if you earn $100,000 per year before retirement, you'd want to have enough savings and other income sources to provide about $80,000 per year in retirement.

This benchmark assumes that you'll have fewer expenses in retirement, such as no longer needing to save for retirement or pay work-related costs. However, it's important to consider that some expenses, like healthcare, may increase.

The $1 Million to $2 Million Target

Some people aim for a retirement savings target between $1 million and $2 million. A survey by Northwestern Mutual found that U.S. adults, on average, believe they'll need $1.46 million to retire comfortably.

Even though $1 million or more can be a big nest egg, you should think about your own situation. Factors like your cost of living, health, and retirement goals can greatly impact how much you'll need.

How to Calculate Your Personal Retirement Number?

Now that you have a general idea of retirement savings benchmarks, it's time to dig into your unique retirement number. While rules of thumb can be helpful, they don't consider your specific circumstances and goals. Here's how to calculate a retirement savings target tailored to you:

1. Estimate Your Annual Retirement Expenses

Start by estimating your annual retirement expenses. Take a look at your current lifestyle and how it might change. Will your mortgage be paid off? Do you plan to travel more? Be sure to factor in healthcare costs, which can add up.

2. Factor in Inflation

Over time, inflation erodes the purchasing power of your money. The U.S. inflation rate has averaged around 3% per year over the long term. When estimating your future expenses, account for this inflation rate.

For example, if you need $50,000 per year in today's dollars and you plan to retire in 20 years, you'll actually need around $90,000 per year, assuming a 3% annual inflation rate.

3. Consider Your Retirement Income Sources

Next, consider all your potential retirement income sources. These might include:

Social Security

Pensions

Part-time work

Rental income

Royalties

Other passive income streams

Subtract your estimated annual retirement income from your estimated annual expenses. The difference is what you'll need to cover from your personal savings and investments.

4. Use a Retirement Calculator

Retirement calculators can do the heavy lifting for you. They take into account factors like your current age, retirement age, life expectancy, estimated expenses, and projected investment returns to give you a personalized savings target.

Many financial institutions offer retirement calculators. For example, Vanguard's retirement income calculator lets you input detailed information about your situation and goals to get a customized retirement savings plan.

Early Retirement: What Else Could Add Up?

Retiring early might sound like a dream come true, but it's not a decision to be made lightly. Before you retire early, there are a few things to consider.

1. Increased Savings Requirements

One of the biggest challenges of early retirement is ensuring you have enough savings to last for a potentially longer retirement period. If you retire at 55 instead of 65, that's an extra decade of expenses you'll need to cover without the benefit of a steady paycheck.

For example, if you plan to retire at 55, you should aim to save at least 7 times your annual income (based on Fidelity's benchmark) to support a comfortable lifestyle in retirement.

2. Healthcare Considerations Before Medicare Eligibility

Another major factor to consider is healthcare. Most Americans become eligible for Medicare at age 65. If you retire before then, you'll need to find an alternative way to cover your medical expenses.

Private health insurance can be costly, especially if you have pre-existing conditions. Based on eHealth's study of ACA plans, ACA plans cost an average of $456 per individual and $1,152 per family per year. This expense can quickly eat into your retirement savings.

3. Potential for a Longer Retirement Period

Early retirement means your savings will need to stretch over a longer period. If you retire at 55, you could be looking at a retirement period of 30 years or more. This means your savings will need to last longer and be able to weather market fluctuations and inflation over an extended period.

How to Plan for the Different Phases of Retirement?

Retirement experience isn't the same for everyone. Typically, it happens in several distinct phases, each with its own financial considerations and lifestyle choices. Let's explore these phases and how to plan for them effectively.

The Go-Go Years

In the first few years of retirement, which are often called the "Go-Go" phase, people are usually very busy and excited. When people retire, they are no longer limited by their work schedules. They often go on new adventures, pursue hobbies, and spend quality time with their loved ones.

However, this increased activity often comes with higher expenses.

To plan for this active phase:

Create a detailed budget that accounts for travel, leisure activities, and potential surprises.

Maintain a strong emergency fund to cover unexpected costs.

Review your investment portfolio to ensure it aligns with your retirement goals and risk tolerance.

The Slow-Go Years

As retirees enter their mid-70s and beyond, the "Slow-Go" phase begins. Priorities often change, and people start to think about living a more relaxed life, possibly downsizing, and being close to their families.

During this stage, housing and transportation costs may decrease, but healthcare expenses start to rise.

To get through this phase:

Consider long-term care insurance to help cover potential future healthcare costs.

Re-evaluate your budget to account for changing spending patterns.

Stay engaged with your community and maintain social connections for overall well-being.

The No-Go Years

The final stage of retirement, the "No-Go" years, typically begins around age 80 and beyond. This phase often necessitates increased medical attention and potential long-term care.

To prepare for this stage:

Explore long-term care insurance options, ideally in your 50s or 60s when premiums are lower.

Discuss your preferences and wishes with family members.

Research long-term care facilities and in-home care options in your area.

So, What Exactly Do You Need to Retire?

It's pretty clear that the amount you need to retire comfortably is different for everyone. But we can give you a general idea and some important things to think about.

For the average person who wants to retire between 60-70 and live a comfortable life, most people seem to be aiming for a retirement nest egg of $1-2 million. This assumes you'll withdraw 3-4% of your savings each year, which many people think is a safe place to start.

But a few things can change this amount:

If you're planning to retire early, like in your 40s or 50s, you'll probably need to save more, maybe $2-3 million or more, since your retirement will be longer.

If you're dreaming of a fancy retirement with lots of travel or expensive hobbies, you might need to aim for the higher end of that range or even more.

How much it costs to live where you want to retire makes a big difference. $1 million will go a lot further in a cheaper area than in an expensive city.

It's important to think about potential health costs and long-term care needs, as these can quickly eat up your retirement savings.

At the end of the day, the most common target people seem to be aiming for is around $2 million for a comfortable retirement. This amount, plus Social Security benefits and any other income you might have, like from a pension or rental property, can give you a good foundation for a happy retirement.

But remember, retirement planning is personal. Things like your age, income, how much you're saving, how your investments perform, and your specific retirement goals all play a big role in figuring out your unique retirement number.