Budgeting—it's a topic that can make even the most confident person feel a bit uneasy. Even high-earners find themselves financially stressed at the end of each month. The truth is that many of us live our financial lives without a clear plan, hoping things will somehow work out. This can lead to overspending, debt, and missed financial goals.

The good news is that you can control your personal finances by making a budget. You might think of it as restrictions, but it's simply a way to understand your money flow and make informed decisions.

So, if you want to sleep better at night knowing your finances are in order, this guide will help you understand all the aspects of budgeting. Let’s get to your financial freedom.

What is a budget?

What is a budget?

A budget is a financial plan that details how much money you expect to earn and how you plan to spend it over a specific period, usually a month or a year.

It allows you to allocate funds for different purposes, such as daily living expenses, savings, and investments.

Essentially, a budget gives every dollar a job to make sure you can meet your needs, wants, and financial goals. It's about spending smart and prioritizing what matters to you.

Why is budgeting important?

With the cost of living on the rise and economic challenges, the need for effective budgeting has never been more critical. Having a clear financial plan and feeling confident about your future sounds great, doesn't it? However, many people don't have a clear financial plan and suffer from stress and financial uncertainty.

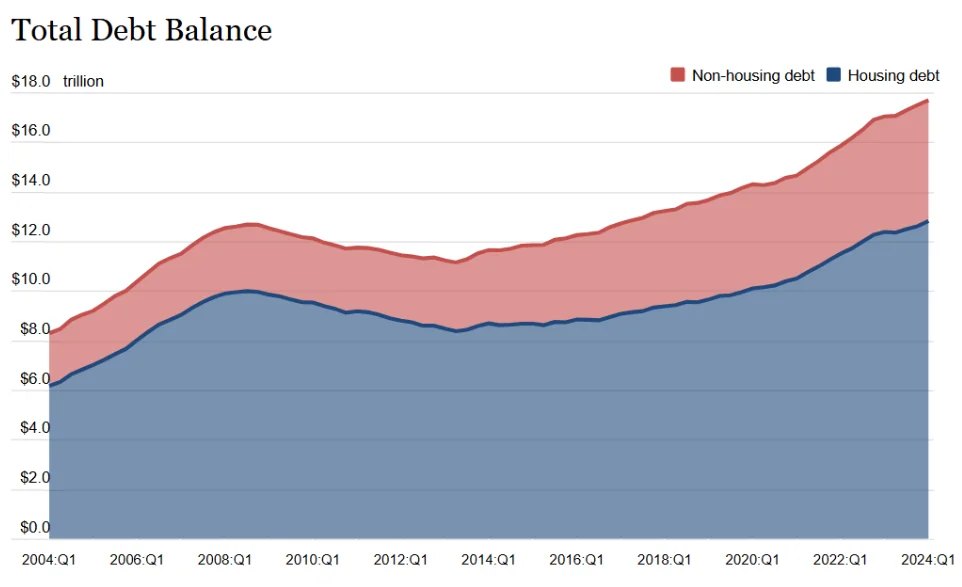

The Federal Reserve reports that U.S. total household debt rose by $184 billion to reach $17.69 trillion. This highlights the importance of budgeting to manage and reduce debt effectively.

Let's look at the reasons you should have a budget:

1. Controlling Your Spending Habits

Budgeting helps you keep a close eye on your daily spending. Without a budget, it’s easy to lose control and overspend. For example, seemingly small expenses—like those 30 Chipotle burritos a month—can add up significantly. When you know exactly how much money is coming in and where it's going out, you can identify areas to cut back and allocate funds to what truly matters.

2. Staying on Track for Financial Goals

Setting goals is easy, but achieving them requires discipline. A budget provides a clear plan and keeps you focused. You can plan how much you need to save each month to reach those goals. Whether it’s saving for a car or vacation, budgeting helps you stay on course.

3. Emergency Preparedness

Life is unpredictable, and unexpected expenses can arise at any moment. A budget helps you build an emergency fund, which should ideally cover three to six months of living expenses. This fund provides peace of mind and financial security during tough times, like job loss or medical emergencies.

4. Managing Debt

Debt can be a real drag on your finances, but setting limits on spending and prioritizing debt repayment can prevent the cycle of accumulating high-interest debt. This proactive approach makes it easier to stay on top of payments and gradually reduce what you owe.

5. Building Financial Stability

Overall, budgeting creates a solid foundation for your financial future. It helps ensure that you can pay your bills on time, save for big purchases, and prepare for retirement. By sticking to a budget, you position yourself for a more secure financial life.

What Are the Different Types of Budgeting Methods?

You can approach budgeting in a variety of ways. Some can be very simple and straightforward, while others can be complex and detailed. Understanding these methods can help you choose the one that fits your needs best. Here are some popular methods.

1. Zero-Based Budgeting

With zero-based budgeting, you start from scratch each month. You list all your income and then assign every dollar to a specific expense, savings, or debt repayment until you reach zero. This method helps you see where your money goes and encourages you to think carefully about each expense.

Let's say you earn $4,000 a month, You might allocate $2,000 to needs, $1,000 to wants, $500 to savings, and $500 to debt repayment. Every dollar is accounted for.

Pros:

Forces you to prioritize spending.

Helps identify unnecessary expenses.

Cons:

Can be time-consuming each month.

Requires careful tracking.

2. 50/30/20 Budgeting Rule

This method divides your income into three categories: needs, wants, and savings. You spend 50% on needs, 30% on wants, and 20% on savings or debt repayment. It’s simple and gives you a clear structure.

For example, if you make $3,000 a month, you'd aim to spend:

$1,500 on needs (like rent and groceries)

$900 on wants (like dining out and entertainment)

$600 on savings and debt

Pros:

Easy to follow.

Flexible and adaptable to different incomes.

Cons:

May not fit everyone’s financial situation perfectly.

Needs adjustments based on individual goals.

3. Envelope System

The envelope system is a fun and visual way to budget. You take cash for each category of spending (like groceries, entertainment, etc.) and put it in separate envelopes. When the cash in an envelope is gone, that’s it for that category until the next month.

For example, if you budget $200 for groceries, you place $200 in an envelope labeled "groceries." When the envelope is empty, you stop spending on groceries for the month.

Pros:

Helps control spending.

Makes budgeting tangible and straightforward.

Cons:

Not practical for online payments or bills.

It requires discipline to stick to cash limits.

4. Incremental Budgeting

This method is often used by businesses but can work for personal finance too. You start with last year’s budget and make small changes based on what you expect for the coming year. It’s great for maintaining stability.

Pros:

Simple and easy to implement.

Good for predictable expenses.

Cons:

May not encourage innovative thinking.

Can overlook necessary changes in spending.

5. Pay Yourself First

This method flips the usual budgeting approach. Instead of paying bills first, you set aside a specific amount for savings or investments right away. After that, you use what’s left for expenses. It’s a great way to ensure you’re prioritizing your financial goals.

Pros:

Encourages saving and investing.

Reduces the temptation to spend savings.

Cons:

It requires discipline to stick to savings goals.

May lead to tighter budgets for expenses.

6. Line-Item Budgeting

This method involves listing every single expense in detail. You categorize them into fixed and variable costs. It’s often used by businesses but can work for personal finance too. This way, you can see exactly where your money is going.

Pros:

Provides a clear view of spending.

Helps identify areas to cut back.

Cons:

Can be overwhelming with too much detail.

Requires regular updates and tracking.

How Can You Start a Budget?

Making a budget might seem overwhelming, but it can be simple and even fun! Let's break down the steps.

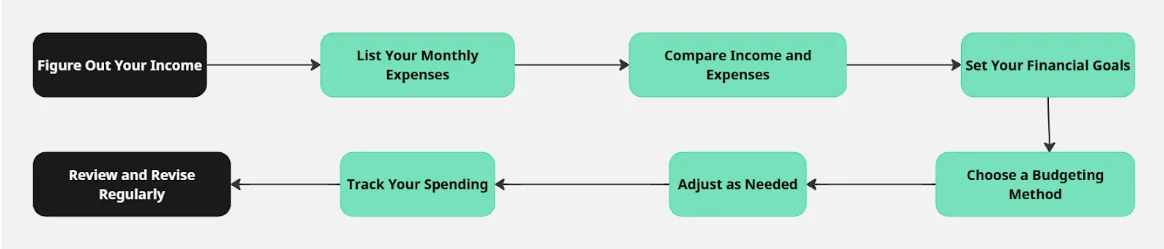

Step 1: Figure Out Your Income

First things first, you need to know how much money you have coming in each month. This is called your net income, which is what you take home after taxes and other deductions.

For example, If you earn $3,000 a month from your job, that’s your starting point. If you have side gigs or other income sources, add those in, too. Let’s say you make an extra $200 from freelance work. Your total monthly income would be:

3,000+200=3,200

So, your net income is $3,200.

Step 2: List Your Monthly Expenses

Next, you need to write down all your monthly expenses. These can be fixed costs (like rent or mortgage) and variable costs (like groceries or entertainment).

Common Expenses to Consider:

Fixed Expenses: Rent/Mortgage: $1,200

Variable Expenses:Groceries: $400

Add these up to see how much you spend each month:

1,200+300+200+400+150+200+100=2,550

So, your total monthly expenses are $2,550.

Step 3: Compare Income and Expenses

Now, it’s time to see how your income stacks up against your expenses. Subtract your total expenses from your net income:

3,200−2,550=650

This means you have $650 left over each month. Great job! This leftover money can be used for savings, paying off debt, or fun activities.

Step 4: Set Your Financial Goals

With your budget in place, think about what you want to achieve financially. Do you want to save for a vacation, pay off credit card debt, or build an emergency fund? Setting clear goals will help you decide how to use that leftover money.

For example:

Save for a vacation: $300/month

Pay off credit card debt: $200/month

Build an emergency fund: $150/month

Step 5: Choose a Budgeting Method

Now that you know your income, expenses, and financial goals, it’s time to choose a budgeting method that fits your lifestyle. For example, if you struggle with overspending, the envelope system might be a good fit. If you prefer simplicity, the 50/30/20 rule could work well.

Step 6: Adjust as Needed

As you start following your budget, you might find that some expenses are higher or lower than you planned. That’s okay! Adjust your budget as needed to reflect your actual spending.

For example, If you find you only spend $100 on entertainment instead of $200, you can reallocate that extra $100 to savings or debt repayment.

Step 7: Track Your Spending

To stick to your budget, keep track of your spending. You can use a simple notebook, a spreadsheet, or a budgeting app. Record your expenses regularly to see how well you’re following your budget.

For example, If you go out for dinner and spend $50, write it down immediately. This will help you stay aware of your spending habits.

Step 8: Review and Revise Regularly

At the end of each month, review your budget. Did you stick to it? What worked well, and what didn’t? Make adjustments for the next month based on your findings.

For example, If you consistently overspend on groceries, consider meal planning or find ways to cut costs, like using coupons or buying in bulk.

What are Common Budgeting Mistakes to Avoid?

1. Not Saving for Emergencies

One of the biggest budgeting blunders is neglecting to set aside money for unexpected expenses. Life is unpredictable, and emergencies—like car repairs or medical bills—can pop up when you least expect them. In fact, over half of Americans don’t have enough savings to cover a $1,000 emergency expense.

How to Avoid It: Start by creating an emergency fund. Treat your emergency fund as a regular expense. Aim to save 3-6 months' worth of living expenses to cushion against financial shocks.

2. Not Tracking Your Spending

Failing to monitor your daily expenses can lead to overspending and an inaccurate budget.

How to Avoid It: Keep a detailed record of all your transactions. Use apps or a simple spreadsheet to track where your money goes. This way, you can adjust your budget as needed and avoid unexpected shortfalls

3. Being Unrealistic

It’s great to be ambitious, but setting goals that are too high can lead to burnout and disappointment. If you try to cut your spending drastically or save a huge amount each month, you might find it hard to stick to your budget. For instance, if you aim to save 50% of your income but only manage to save 10%, you may feel discouraged.

How to Avoid It: Set realistic and achievable goals. Break larger goals into smaller, manageable steps. Instead of aiming to save a large sum immediately, focus on saving a little each month. Celebrate your progress, no matter how small, to keep yourself motivated.

4. Overestimating Available Funds

It’s easy to think you have more money to spend than you actually do, especially if you aren’t tracking your expenses closely. This can lead to overspending and financial stress. For example, if you base your budget on your gross income (before taxes) instead of your net income (what you take home), you might find yourself short on cash at the end of the month.

How to Avoid It: Always budget based on your net income. Keep a close eye on your spending by tracking every expense, no matter how small. Consider using budgeting apps or tools that can help you monitor your cash flow. This way, you’ll have a clearer picture of your financial situation and avoid the disappointment of running out of money.

5. Forgetting to Adjust Your Budget

Life changes, and so do your financial needs. It can be a new job, a growing family, or unexpected expenses; your budget should evolve with your circumstances. Sticking rigidly to an outdated budget can lead to frustration and overspending.

How to Avoid It: Revisit and adjust your budget quarterly or whenever a significant change occurs, such as a salary increase, moving to a new home, or having a baby. This helps ensure your budget stays aligned with your current financial situation

6. Missing Bill Payments

Failing to make payments on time can lead to late fees and unnecessary stress. If you’re manually paying bills each month, it’s easy to forget a due date.

How to Avoid It: Set up automatic payments for your regular bills. This way, you won’t have to worry about missing payments, and you can focus on managing your budget without the added pressure of remembering due dates.

7. Ignoring Small Expenses

Small purchases can add up quickly and derail your budget. Many people overlook these little expenses, thinking they don’t matter much. However, those daily coffee runs or picking up snacks at the gas station can significantly impact your overall spending.

How to Avoid It: Track every single expense, no matter how minor. You might be surprised at how much those small purchases accumulate over time. Consider creating categories for discretionary spending and setting limits for each category to help keep your spending in check.

8. Not Making a Plan to Pay Off Debt

Without a clear strategy to tackle debt, you might end up paying more in interest and extending your debt period.

How to Avoid It: Use methods like the debt snowball (paying off the smallest debts first) or debt avalanche (paying off debts with the highest interest rates first) to systematically reduce your debt.

What Are the Best Budgeting Tools and Resources?

Creating and sticking to a budget is much easier with the right support. There are tons of tools and resources available to help you manage your money effectively. Here are some of the best budgeting apps, templates, and resources available in 2024.

Budgeting Apps

Rocket Money - Helps manage subscriptions, track spending, and negotiate bills to save money.

YNAB (You Need A Budget) - Uses a zero-based budgeting approach to ensure every dollar has a job.

Simplifi by Quicken - A comprehensive app that provides a holistic view of your finances, from spending insights to investment tracking.

Honeydue - Honeydue is designed for couples to manage their finances together. It allows partners to share budgets, track expenses, and communicate about their finances.

PocketGuard - PocketGuard simplifies budgeting by showing how much disposable income you have after accounting for bills and savings goals.

Budgeting Books

"The Total Money Makeover" by Dave Ramsey - A classic guide that teaches a simple, proven method for getting out of debt and building wealth.

"Your Money or Your Life" by Vicki Robin and Joe Dominguez - A transformative book that helps you reframe your relationship with money and achieve financial independence.

"The 30-Day Money Cleanse" by Ashley Feinstein Gerstley - A practical book that provides a step-by-step plan for taking control of your finances in just one month.

Budget Worksheets and Templates

Google Sheets Budget Templates - Free, customizable templates such as 50/30/20 rule spreadsheet and finance worksheets.

Microsoft Excel Budget Templates - Various templates for different needs, from simple budgets to detailed financial plans.

Vertex42 Printable Budget Worksheets - Printable worksheets for tracking expenses on paper.

Budget Templates from Canva - Customizable and visually appealing budget templates.

Budgeting Courses

Coursera - Offers a variety of personal finance courses, including "Personal & Family Financial Planning" from the University of Florida.

Udemy - Has a wide selection of budgeting and money management courses, ranging from beginner to advanced levels.

Skillshare - Provides classes on budgeting, saving money, and achieving financial goals, taught by experts in the field.

The Takeaway

At first, making a budget might seem hard, but it gets easier with practice. By setting up a plan for your income and expenses, you can save for your goals and avoid stress about money.

Here are some closing tips:

Begin with a simple budget and adjust as you go.

Review and update your budget strategy regularly.

Life changes, so be ready to tweak your budget as needed.

Acknowledge your progress, no matter how small.

Remember, budgeting is about making your money work for you. Start today and watch your financial health improve!